July 20, 2025/

No Comments

In today’s complex and fast-paced business world, effective leadership is no longer a luxury—it’s a necessity. Companies that invest in...

In today’s complex and fast-paced business world, effective leadership is no longer a luxury—it’s a necessity. Companies that invest in...

Yes, Kids Can Make Real Money in 2025 Gone are the days when lemonade stands and lawn mowing were the...

Why Selling Digital Products Is Booming In the digital age, selling digital product is one of the smartest ways to...

The Work Revolution You Might Already Be Part Of The Gig Economy is transforming how people work around the world....

Is Now a Good Time to Open a Hair Salon? Absolutely. Despite economic shifts and tech trends, hair salons remain...

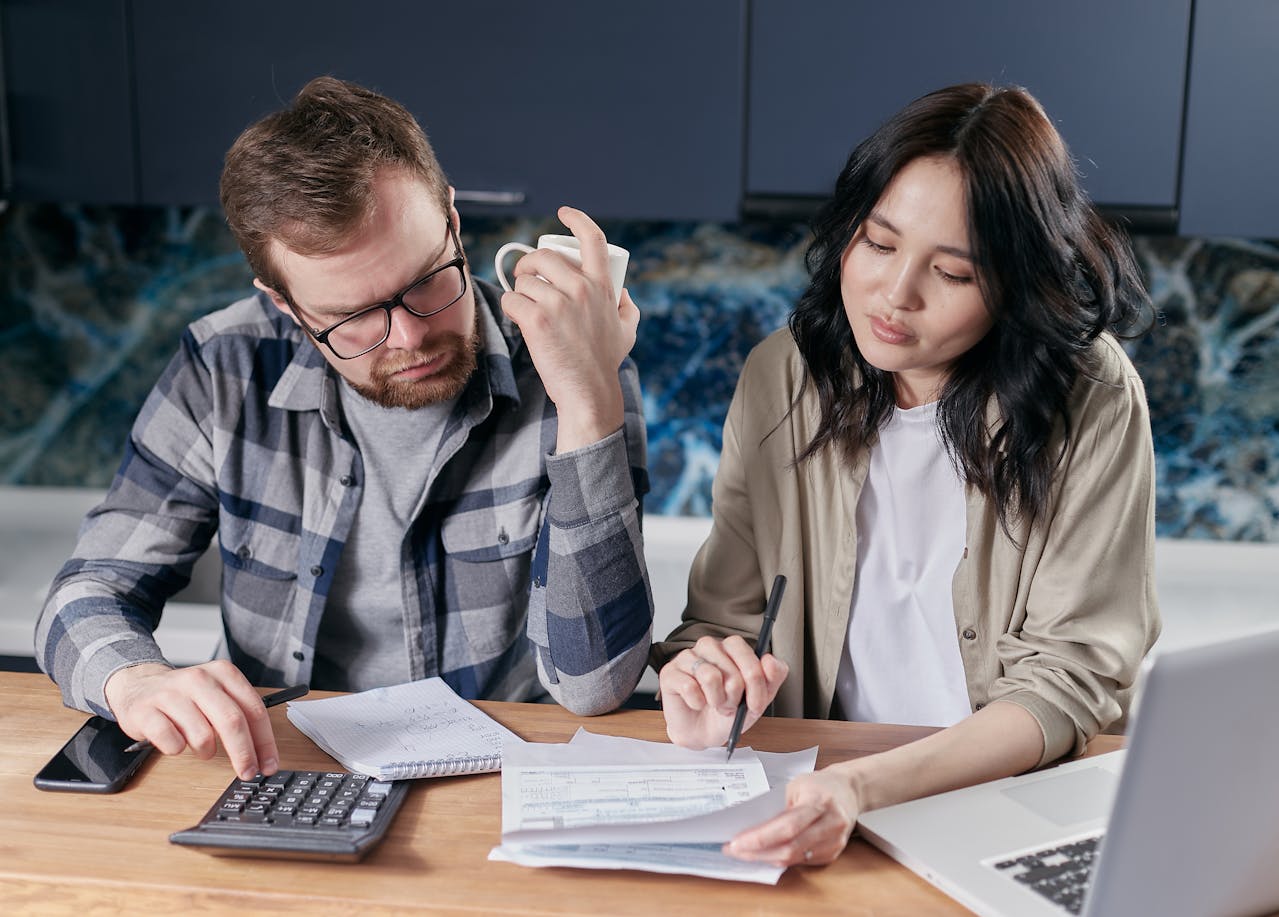

Starting a Small Business? Let’s Talk Money Starting a small business is an exciting leap—but financing it? That’s where many...

Spending Smart Isn’t Always Spending Less In today’s world, most people associate “saving money” with spending less or buying the...

Gaming Has Gone Pro and Profitable Gaming used to be seen as just a hobby. But today, it’s a billion-dollar...

Let’s face it—YouTube is more than just a platform for watching funny cat videos. It’s become one of the most...

If you’ve ever browsed a blog or watched a video online, chances are you’ve seen Google ads. These aren’t just...

If tax season has crept up on you and you’re not quite ready to file, you’re not alone. Every year,...

Many Americans opt to claim early Social Security benefits at age 62 to gain immediate income. However, doing so can...